Beating inflation with compound interest investing strategy

Beating inflation with compound interest investing strategy

Losing money to inflation?

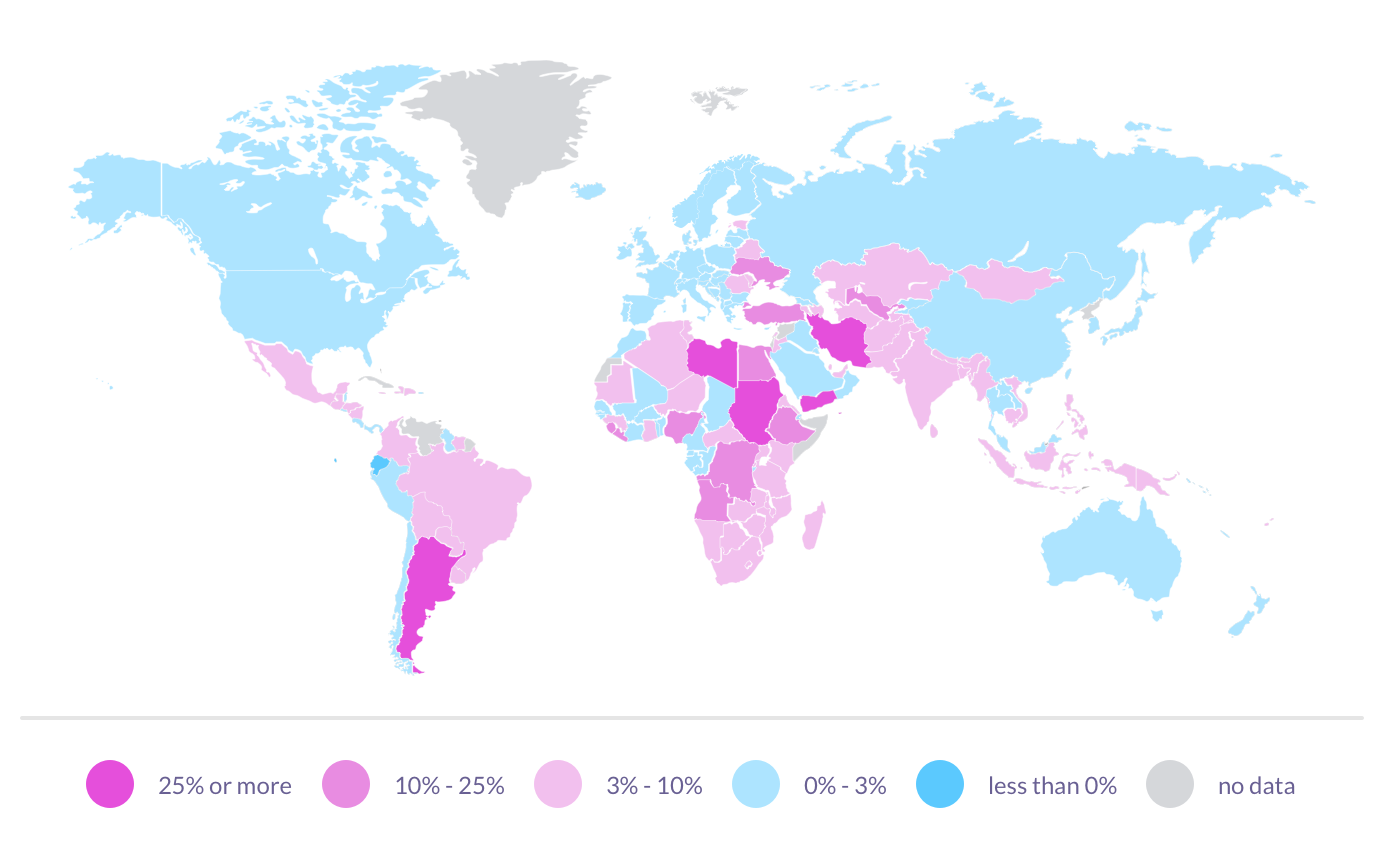

It is a proven fact that the amount of money you have today is worth more than it will be in the future and in places like Venezuela or Zimbabwe, unfortunately, your money, eventually, becomes worthless. This happens due to a process of inflation, which is a devaluation of the value of your money over the time. If not invested, your money will buy less than it can today. You do not have to be super smart to understand that as prices in shops rise sooner or later and you have to pay more for the goods you consume on a regular basis. Just to give you a current inflationary picture in different regions of the world in 2018 we have put you a world map of annual inflation from IMF (International Monetary Fund) to see how much value money loses in various parts of the world each year.

Data source: IMF DataMapper

The numbers may not look alarming to you, but if you do basic calculation you will find out that if prices stay the same for a prolonged period of time, consumer goods in Central Asia and Caucasus (the highest level of inflation) will double in price every 8 years and in Europe (the lowest level of inflation) every 45 years. Despite the fact, the inflation stays low in Europe for the time being, if an average young person living in the region does not find a way to increase his income he will find his financial well-being drastically diminished by the time he reaches the age of retirement. How can we preserve our money and possibly increase it while living in an inflationary economic environment?

Investing in financial instruments with the best annual returns

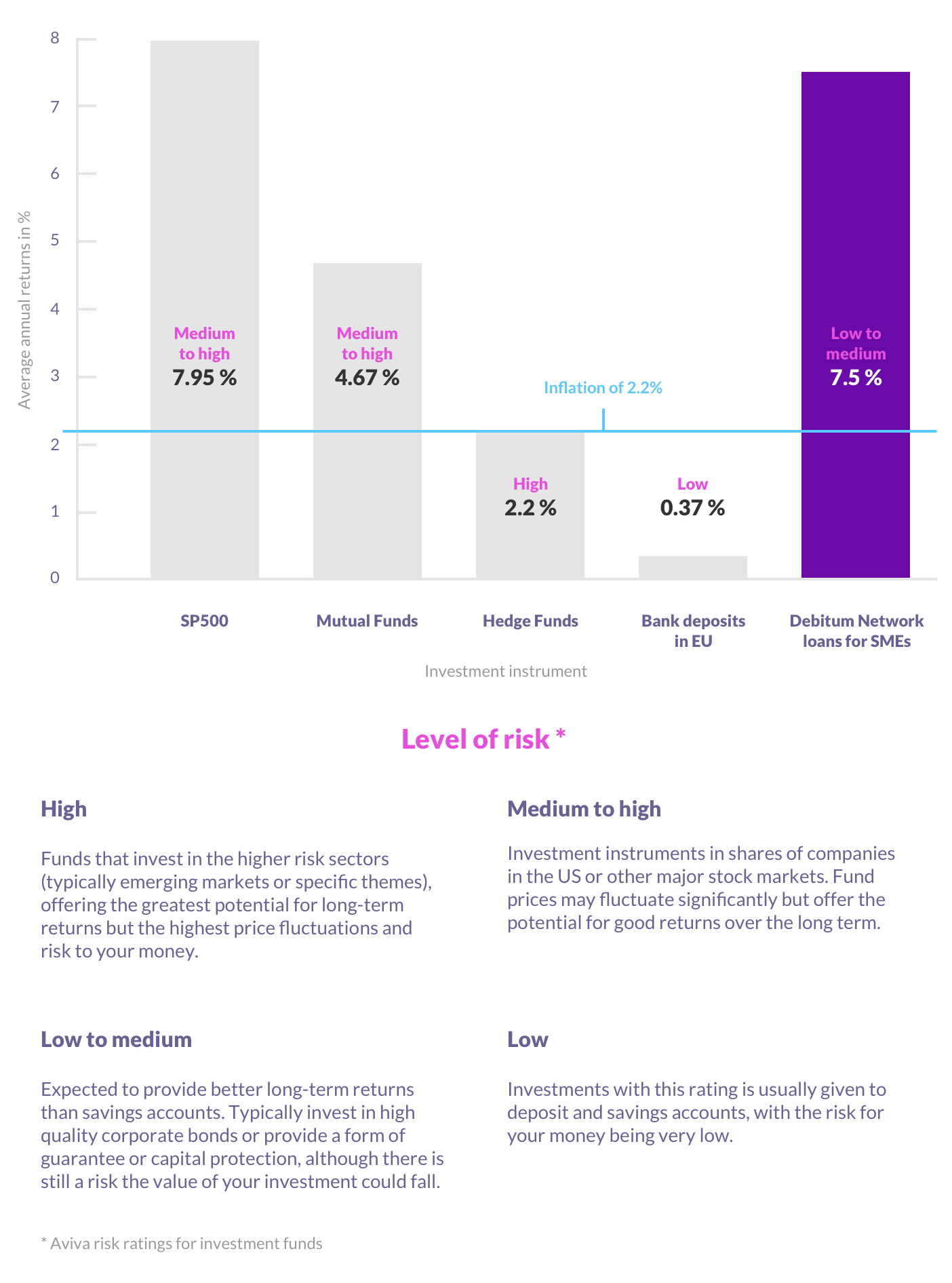

Most economists and financiers agree that investing is a way to preserve your capital from losing value to inflation. Market analysts and experts try to single out the best investments out there that could beat inflation and put an investor ahead of it. For quite some time, the most popular investment options have been SP500, mutual funds and hedge funds. Let’s see how well those perform annually and also add two more investment options: average interest rates for keeping money in a bank in EU as well as investing in short-term loans at our own Debitum Network platform and we also added a risk level for each instrument (used by Aviva group to evaluate risk of investment funds). Then, let’s try to figure out how each instrument performs in relation to inflation in the least inflationary economic area the European Union where annual inflation on average is 2.2%.

Comparing the numbers in the chart with the inflation in the least inflationary region of Europe we learn the following: keeping money in savings accounts in a bank (in EU) will put you in a losing position in terms of inflation. Money invested in hedge funds will help you to stay at break-even with inflation (ironically speaking, this is the riskiest type of investment). You will be 2.6% ahead of inflationary pressure if you put your cash into mutual funds. The best performer in the basket is SP500 that puts your returns well ahead of inflation by 5.75% and the next best option is short term loans on Debitum Network platform helping you to move ahead of inflation by 5.3%.

What if you live in a more inflationary economic area such as Africa, the Middle East or Central Asia? None of the above mentioned investment options would protect your capital from being corroded by inflation. Even the best options indicated in the table above put you behind by around 5% to say nothing of the other less profitable choices like hedge funds or keeping money in a bank. Furthermore, it is obvious that inflation will not stay that low as it is now with very low base rates set by Central banks. It will pick up and an investor will have to search for extra sources to improve on the returns. What could be the best solution to improve the returns keeping risk/reward ratio tolerable? This brings us to the idea, which the legendary scientist Albert Einstein, presumably called “the most powerful force in the universe”. And that power is the ‘compounding interest’. What is it and how does it work?

Investing in financial instruments where interest compound

As opposed to simple interest rate, compound interest rate account earns money, not only on the money invested but also on the accumulated interest of the previous periods.

The formula for compound interest can be calculated in this way:

“Compound Interest = Total amount of Principal and Interest in future (or Future Value) less Principal amount at present (or Present Value) or = [P (1 + i)n] – P

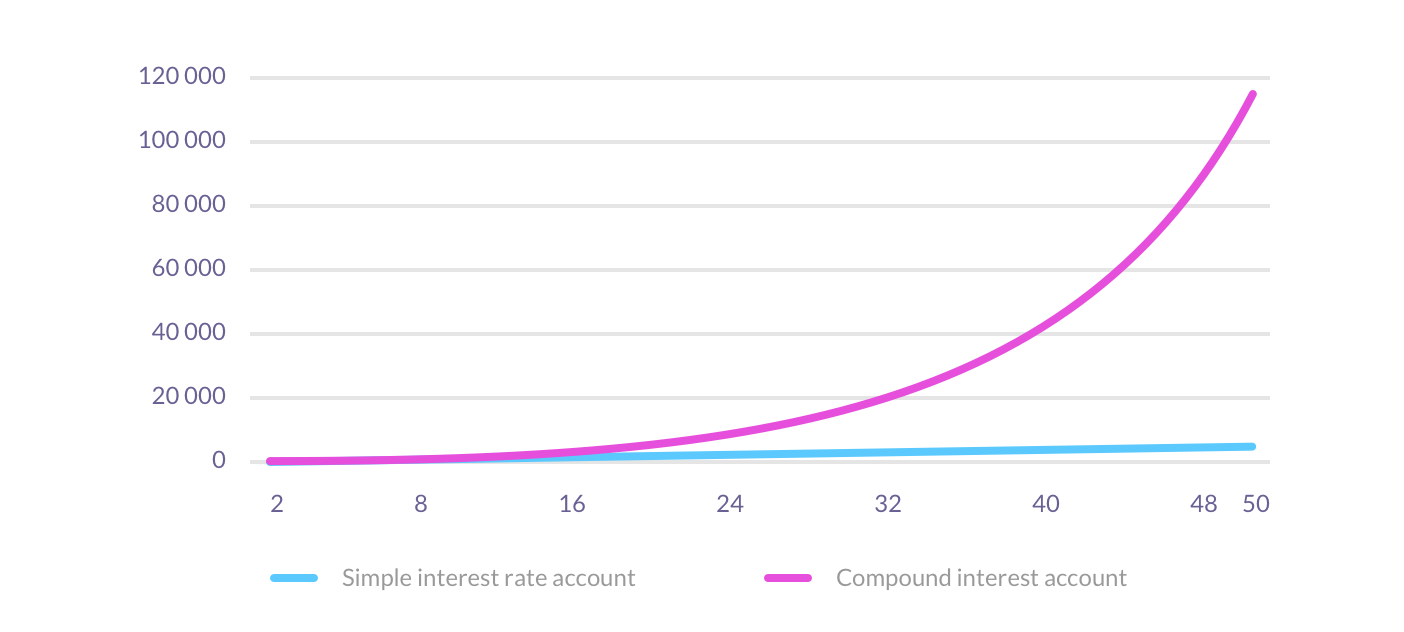

For example, you invest 1,000 Euros at an annual interest of 10% for both simple and compound interest rate (compounded once a year). At the end of the second year, you will have 1,200 Euros on a simple interest rate account and 1,210 Euros on compound interest rate account (compound interval once a year). If that does not look much, look what happens if you keep the money in the account with the same interest (compounded once a year) for 5, 10, 25 and 50 years.

The acceleration of compounding

Looking at the chart above we will arrive at a universal truth, that the sooner you start investing and the longer you do it, the better returns you will achieve due to the tremendous fact of acceleration of compounding. Initially, your simple interest rate account and compound interest rate accounts do not differ much, but as the time goes on we suddenly see a dramatic difference due to interest made on interest year after year. In the long haul, It will put you really far ahead of inflation even in if you live in high inflationary zones.

Increasing compounding intervals

The example above was with the compounding interval once a year. We may take a step further and possibly increase the returns if the compounding interval was set to every month. If we take Debitum Network, where short-term loans are at 7.5% on average you can invest in one month loans and get compounded interest every month. In that case, you will earn an extra 0.25% on the first year of your investment. That may not seem much, but that’s very close to the annual interest rate that you will be offered for your deposit in European banks (on average).

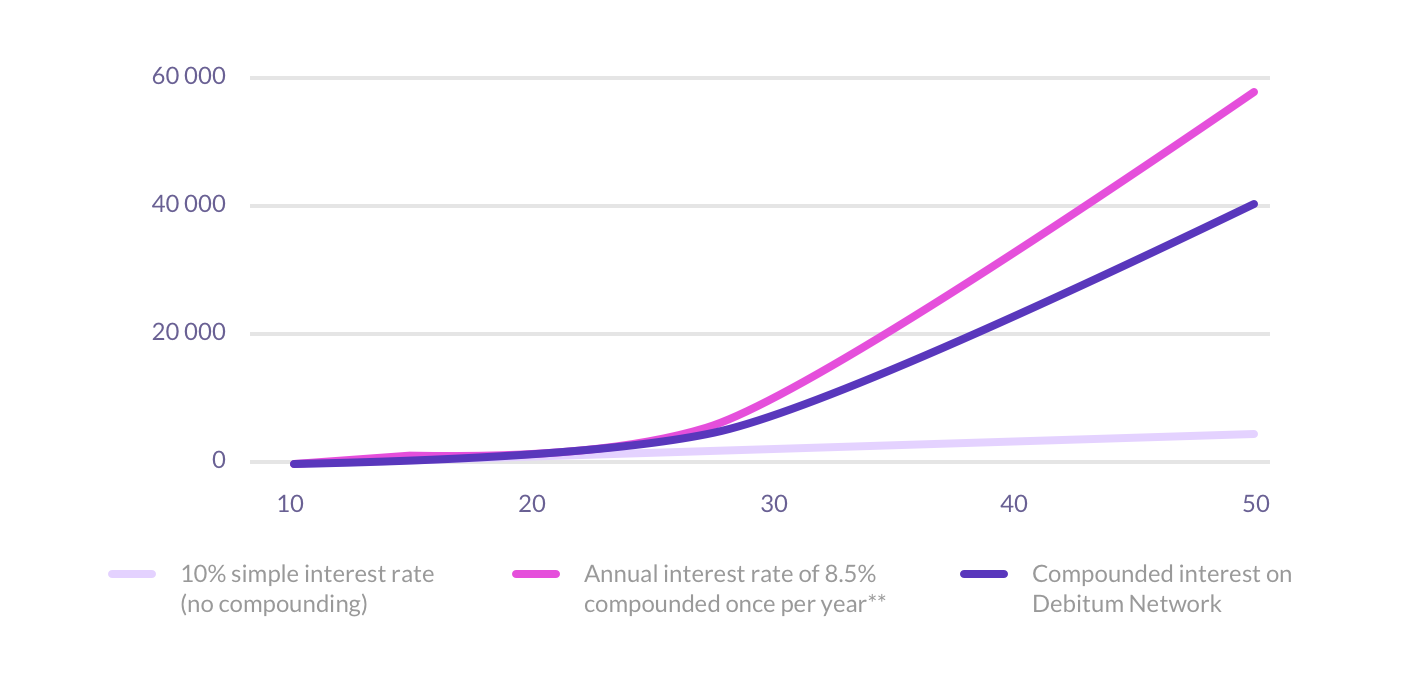

How would you fare if you invested 1000 Euros with Debitum Network at an average 7.5% annual interest rate compounded interval every month, 8.5% compounded once a year and simply put the same amount for 10% simple interest rate into a savings account for 5, 10, 25 and 50 years respectively?

It is interesting to note, that just 1% higher interest rate (8.5%) compounded once a year with a portfolio of 1000 Euros would have done better than portfolio (same amount) with 7.5% (annual interest rate) compounded every month. This shows that the effect of compounding is more powerful over a longer period of time, not the interval of compounding. Similarly, 1% bigger interest matters a lot in the long haul. On the other hand, a portfolio with the higher simple interest rate (not compounded) over a long period of time falls extremely behind in relation to both other portfolios (compounded interest) by 8.2 and 11.6 times respectively at the end of 50 years. This, again, justifies the fact that the earlier you start and the longer you keep your money employed, the larger your portfolio grows and the best part is, that it happens exponentially. Investing in the most popular options such as stock indices, mutual funds or hedge funds does not even offer you a possibility to compound interest the way you can do it with Debitum Network.

Our platform gives you the advantage to pick loans with flexible amounts and duration. So, you can invest monthly and earn interest on both principal and previous interest of the loans, thus compounding interest bit by bit and as time goes on see how your earnings accelerate. We know that investing for 50 or 25 years with one company may seem too far-fetched, but the illustration above is given for the sake of showing you how compounding works and how returns accelerate with each consecutive year. That’s precisely why a smart investor like Warren Buffett believes that starting to invest early and keeping it doing it till you retire will create you a nest egg and make you financially prosperous due to the compounding principle.

Ready to earn compound interest?

The good news is that investing with Debitum Network, not only allows you to earn compound interest, but each loan on our platform carries an additional guarantee (personal guarantee from owners, accepted invoices from large companies or guarantee by another company or a buyback guarantee from a broker), thus making your investments with us less risky. We do believe that safer investments are possible and high returns come with time and with the help of compounding interest, but never at the expense of the safety of your money.

If you want to try our platform and see how you can compound your interest in short-term loans you are most welcome. It does not cost you anything to open an account, we do not have any hidden fees and you can stop investing any time you want.

Disclaimer: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.