Correlation between credit scores and interest rates

Correlation between credit scores and interest rates:

Risk assessors assign a company that borrows a credit score. When businesses apply for capital with lenders a risk score serves as one of the key ratings that define whether the specific borrower is solvent and should be granted a loan or not. A credit score helps lenders understand whether your business is in good shape, how well you fulfill your responsibilities as a borrower, and if your company can make payments on time. The risk rating that a business gets either increases the possibility to get a loan or reduces it. The riskier a company is, the worse credit/risk score it will be assigned. The borrower will also have to pay higher interest rates if a lender approves an application for a loan. There is a correlation between credit scores and interest rates. This is also true for investments on Debitum Network.

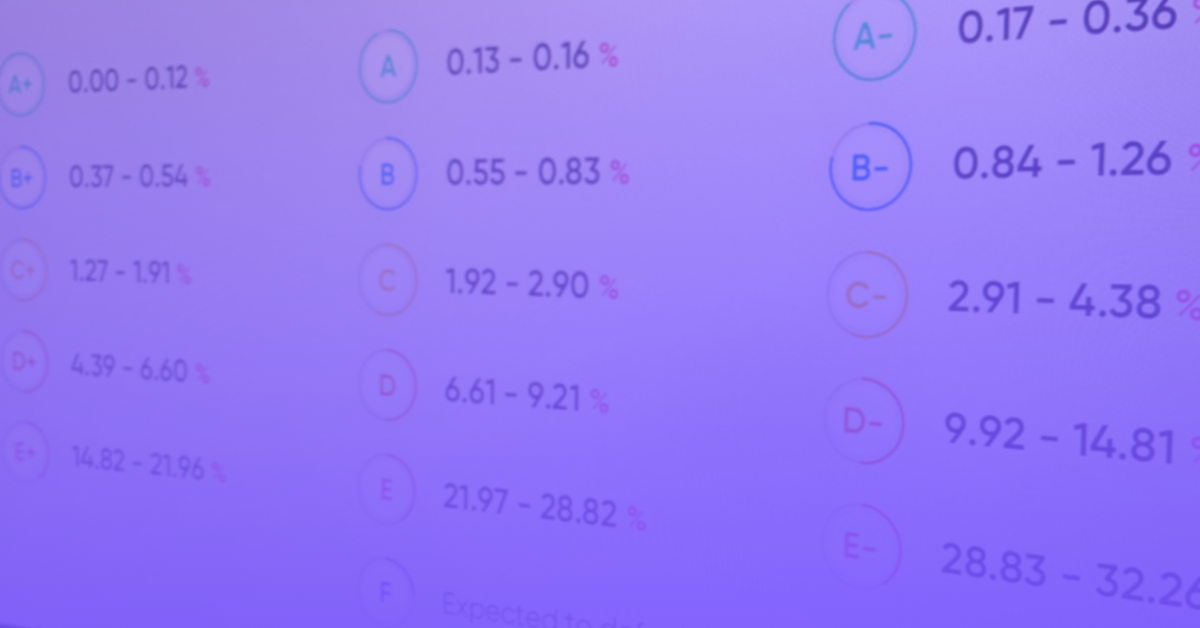

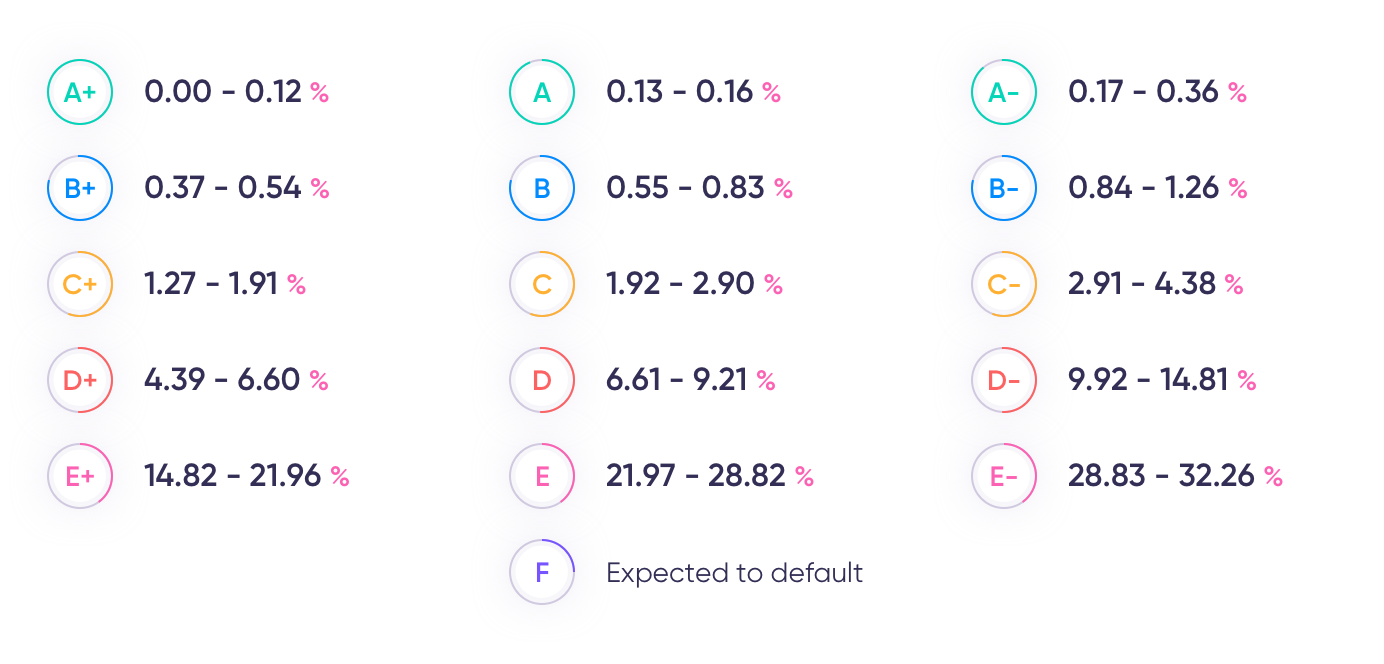

Debitum Network credit score

Credit scores used on Debitum Network are assigned based on a standardized probability of default of the business during the next 12 months. Debitum Network has aligned credit scores received from different risk assessors to fit in the same unified scale. Below is the table with specific credit scores used on our platform.

Correlation between credit scores and interest rates

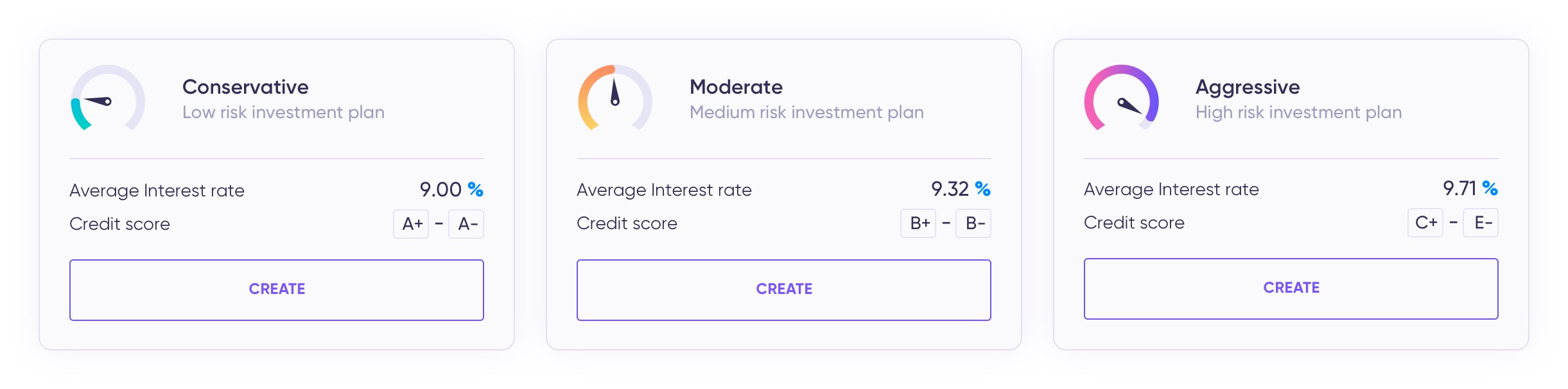

There is a correlation between credit scores and interest rates. A rule of thumb is that the lower the credit score, the higher the interest rates. And vice versa, the higher the credit score, the lower the interest rates. Riskier assets tend to have higher rates and safer ones lower rates. This is true in most situations, the higher the risk, the bigger the returns, and vice versa. Take a look at 3 different investment plans depending on risk tolerance (the example is for illustration purposes, the actual interest rates for various risk classes are dynamic and change) on Debitum Network platform.

Are there any exceptions?

Occasionally, there are. About a year ago, we discussed a situation where credit scores for assets from Local Municipalities of Lithuania were low and what we did about it. Our rationale was detailed in this blog post.

You should also know that loan originators that provide Debitum Network with assets assign specific interest rates for them. So, there might occasionally be some discrepancies between credit scores and interest rates and you can see A- score assets higher interest rates than C score assets (this is just an example).

Thus, you should not be surprised when from time to time you see better interest rates for the assets that have better credit scores than the ones that have worse ones. This is an exception, not the rule!

Trust the score

You should also remember, that risk scoring on Debitum Network is provided by independent risk scoring parties. Debitum Network outsources the job to independent professionals who have years of experience in the field, databases, and other necessary tools to do a precise and trustworthy risk assessment. We decided not to do risk assessment ourselves as generic risk scoring methods are not very precise. Furthermore, using services of independent risk assessors increases transparency, the accuracy of scoring, and gives extra security for investors’ funds.

All assets on Debitum Network carry low risk

Despite the fact, assets on Debitum Network vary from A- to D (there have been 3 E+ assets), all of them are low-risk investment options for investors. Why? We cannot stress it enough, but all the assets uploaded on our platform are business loans. They carry less risk as our borrowers often pledge collateral (assets) to back up their obligations. Secondly, the loans are short term. We ask our loan originators for loans that have short term till maturity. This means that the borrowers have already been paying off principal/interest on those loans. If they did not default on their obligations for a year, or a year and a half, they will most likely not default on them 2-4 months till repayment. Thirdly, most of the loans are protected by a buyback guarantee. It means, that if the borrower is late with repayment by more than 90 days, the broker who issued the loan will have to buy it back with the outstanding principal and interest (18 assets have been bought back since the launch). Last, but not least, we do not accept any assets under F rating as they have a very high probability of default. Assets with D-E ratings must be backed by collateral in order for us to upload them on our platform for investment. There hasn’t been a single default on Debitum Network!

Top asset of the week

You should really consider adding the asset of the week to your portfolio. The borrowing company is a European based distributor of vehicle parts and accessories with a focus on service structure and quality, creating the highest value for the customer in the auto exploitation market. The Company has more than 14 million EUR in revenues, employs more than 80 people, and has been in business for more than 27 years. The purchaser of the invoice is a manufacturer of refined petroleum products, it has more than 22 million EUR in revenues, employs more than 50 people, and has been in business for more than 21 years. The asset is protected by a buyback guarantee. Can it get any better? If you are interested in the asset, you can add it to your portfolio right away.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.