Why don’t banks lend to small businesses and what could be the solution?

Why don’t banks lend to small businesses and what could be the solution?

It is a fact that most businesses go bankrupt within three years after the launch for one major reason – lack of access to credit. International Finance Corporation (under World Bank) research 2 years ago showed an astonishing fact that there was a 2.6 trillion $ credit gap for SMEs. An even more astonishing fact is that after two years the credit gap widened to 5.2 trillion $. This makes it obvious that traditional bank lending to SMEs is broken and has to be fixed. Let’s look at why banks tend not to lend to small businesses and what could be the solution to the problem.

|

Strict regulation |

The post-2008 recession resulted in more strict regulation imposed from Central Banks to commercial ones, which caused commercial banks to rethink their risk tolerance and restructure their loans. It is obvious that small businesses are riskier than large corporations and this is the primary reason banks tend to lend to bigger companies and deny credit to smaller ones.

|

Smaller loans are less profitable |

Larger businesses take larger loans than small businesses do. Naturally, larger loans generate more profit for banks than smaller ones. As a result, banks focus more and more on lending to large corporations and effectively decline 80% of small business applications for loans. A typical small business loan will vary from 20,000 to 100,000 Euros. Banks unwillingly finance loans that are less than 500,000 Euros. It costs banks just as much to underwrite a 500,000 Euro loan as it does a 100,000 Euro loan. Thus, it does not make financial sense for banks to finance small loans.

|

No collateral |

Most banks usually require collateral to give out a loan which acts as a guarantee that the loan will be repaid. The value of the collateral will have an influence on the amount the bank will be willing to lend to a borrower. A lot of small businesses can offer no collateral and thus are often denied the requested funds.

|

Low-risk score or lack of credit history |

Banks carefully study your credit history to evaluate your creditworthiness. If you have bad credit or lack a credit history, the bank will most likely refuse to issue you a loan. A lot of new businesses are too young to have a good credit history, and it becomes an obstacle for them to get loans from the bank.

|

No personal guarantees |

Banks often require personal guarantees from business owners, which makes the owner of a company personally responsible for paying back the loan. This is a risky choice for business owners as in case of failing to pay off the loan they will have to stick to their given guarantee and find the way to pay off the loan from a personal account.

What solution do SMEs have?

Taking into account banks’ approach regarding lending it is quite understandable why they hardly ever lend to SMEs. However, if you are a business owner and your application for a loan keeps rejected, again and again, you want to find an alternative solution. You have to find a way to get funding elsewhere. Fortunately, alternative finance companies have different requirements than banks and it might be much easier for you to get a loan from them. Alternative financing companies that specialize in invoice financing or issuing business loans will most likely accept your application and provide you with necessary funds if you meet the minimum requirements.

Advantages of alternative financing methods in getting SMEs a loan

Loan originators that upload assets on Debitum Network platform are effectively working to fill the credit gap and provide small businesses with the necessary funds. Take, for example, one of our partners (loan originator) Debifo that specializes in invoice financing. Small business owners can take advantage of Debifo financial services and reduce payment term of 30-120 (typical terms to get money from services provided) days to just a few days.

Debifo similarly is more favorable to small businesses at it does not require long term contracts, collateral and it does not have hidden fees for their services. After completing a short registration form, clients can raise invoices for financing and receive the funds they need within a few days. It would take 1-2 weeks to do the same thing with the banks. It is enough for a young company to prove that they have revenues exceeding 30 000 Euros, provide services and goods to other businesses and have been in business at least 6 months, and they will most likely get the necessary funding.

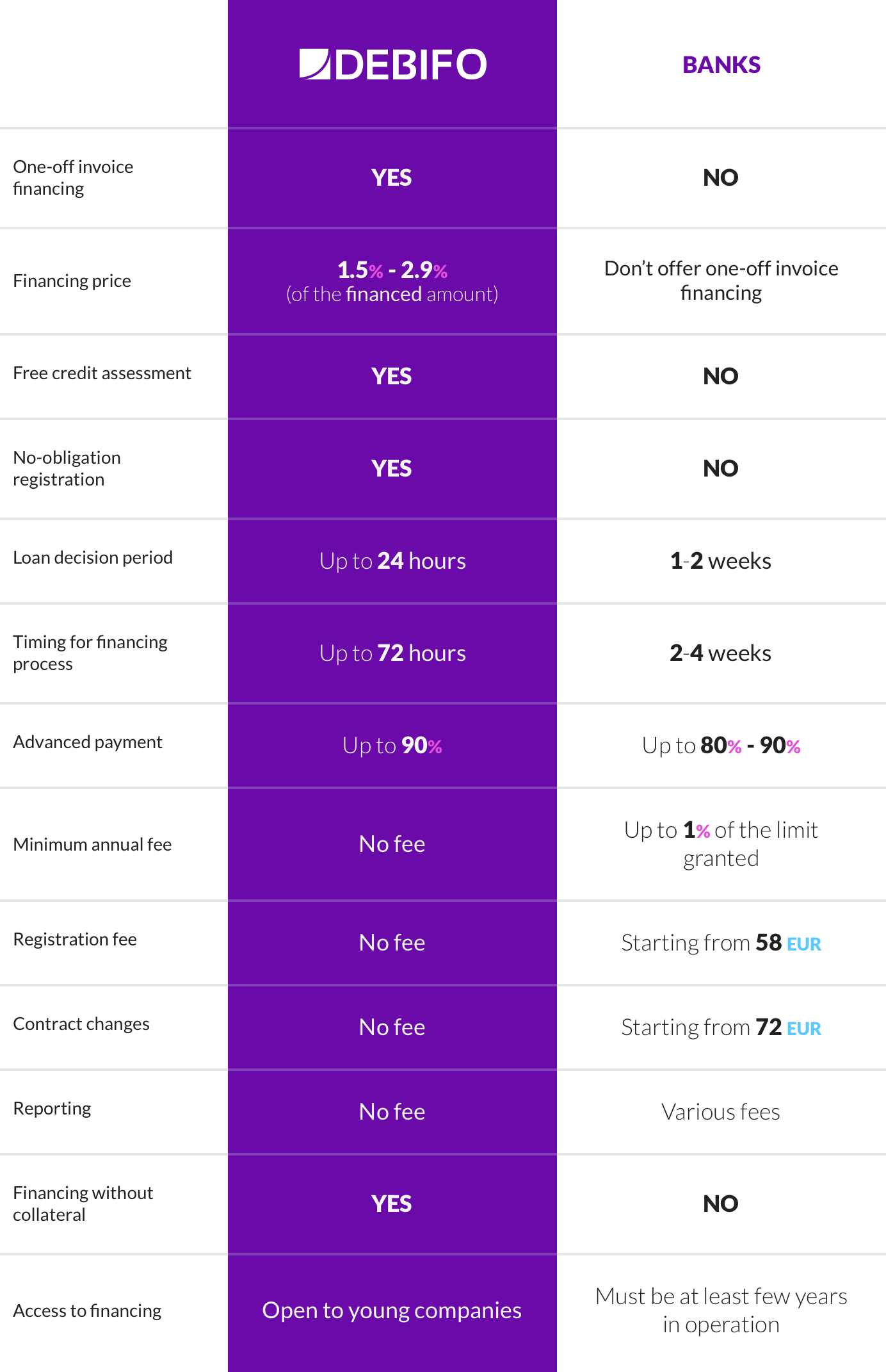

A comparison between Debifo factoring and an average bank factoring

Having looked through the requirements that banks have for SMEs, various fees for services and etc., it becomes obvious why small businesses have difficulty in getting loans from banks. On the other hand, much more flexible conditions from alternative lenders such as our partner Debifo get access to funds for most small companies in a very short period of time and less strict requirements. The solution for SMEs to acquire loans at affordable terms is there, it is alternative finance companies such as our partners Debifo or recently onboared TradeBacking.

Investors can invest in short term loans for SMEs on Debitum Network platform

Debitum Network platform is an excellent choice for those who want to participate in helping SMEs to get funding by investing in short term loans (assets) on the platform and making interest at the same time. The average term of an asset is 53 days and annual interest rates vary from 7% to 11%. Minimum deposit is 50 Euros and the minimum investment amount – 10 Euros. You can use an auto-invest function to distribute your money in chunks and reinvest the earned interest as well as principal making compounding interest as a result.

Ready to try Debitum Network?

Disclaimer: It is important to point out that the approach presented here is not necessarily suitable for everyone and is presented for information purposes only. It is not intended to be investment advice. You should seek a duly licensed professional for investment advice matching your specific situation.