Importance of responsible lending

Importance of responsible lending:

Access to credit is a crucial measure for a lot of businesses to function unhindered and expand. It is a fact that most small companies go bankrupt not because they do not have a business plan, talent, or ambition to pursue their goals, but due to lack of access to credit. Thus, lending is an inseparable factor in the growth of both global and local economies.

However, irresponsible lending has led to a lot of financial and economic problems around the world. One of them was the financial crisis of 2009 when lending institutions were giving loans left and right without taking into account whether individuals and businesses would be able to repay those loans. We know really well what were the consequences of that behavior. In this post, we are going to look through the issues that irresponsible lending creates and give some highlights on how alternative finance platforms can make the process of lending and investing more responsible.

Careless lending causes increase in defaulted loans

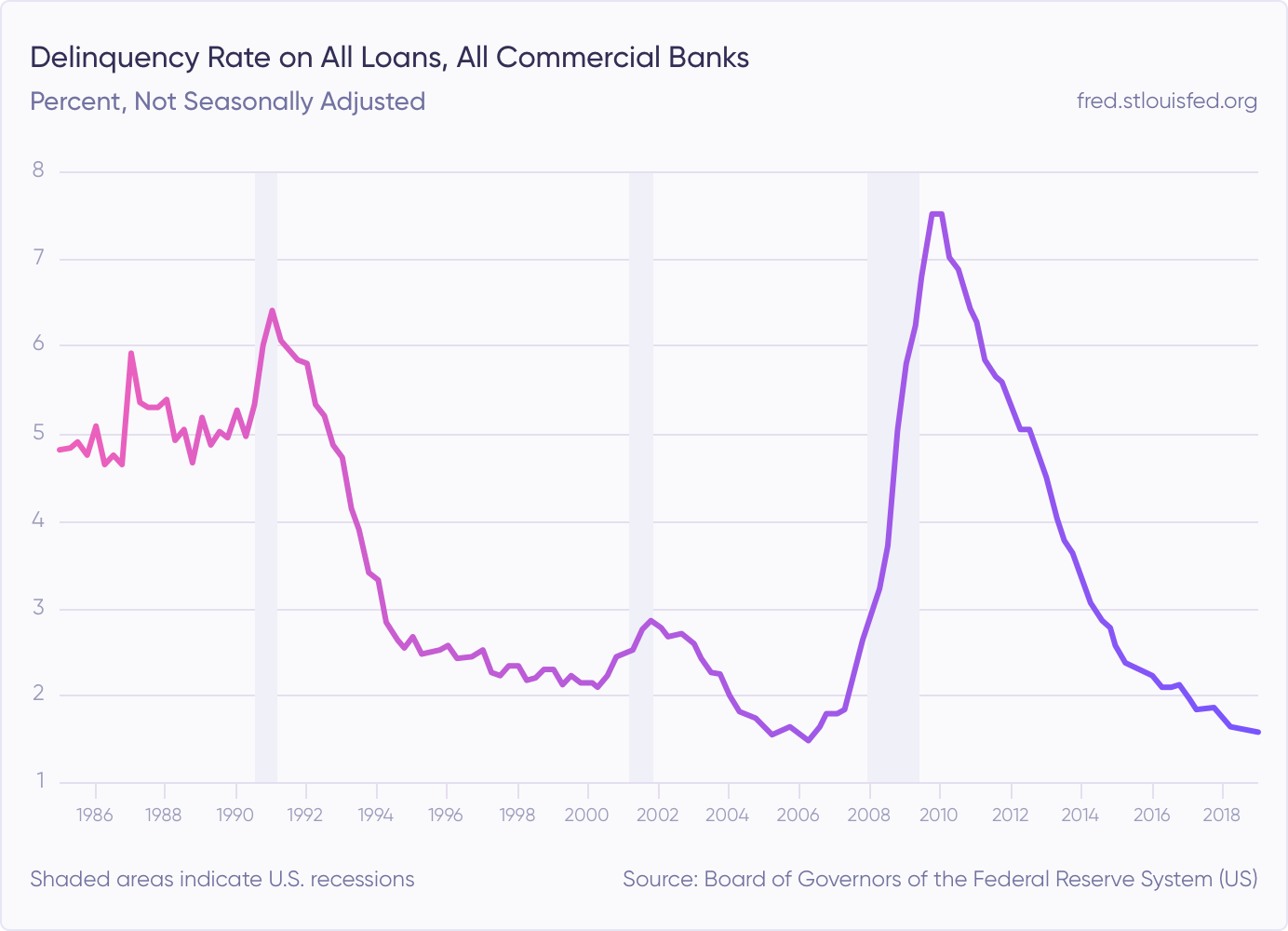

The average loan delinquency rates in commercial banks during the crisis of 2009 reached a peak of 7.5%. It was obvious that lending to whoever asks for a loan can dramatically increase the number of defaults, and cause bankruptcies not only for those who borrow but for those who invest in various financial instruments connected to lending. We saw it in the case of Lehman Brothers who invested heavily in subprime mortgage loans. As a result, people lost their homes, banks ended up having lots of bad debts (some needed a bailout from Central Banks), and investing companies were left holding worthless synthetic assets that irresponsible lending institutions created. The chart below is from the research done by the Federal Reserve Bank of St. Louis. It shows delinquency rates on all loans from all commercial banks in the US. See how the delinquency rates rise during excessive lending cycles.

Source: fred.stlouisfed.org

After the crisis banks became more careful. No more loans with zero initial payment, or collateral to pledge. They check the borrower’s credit history more carefully and ask for more guarantees from businesses and consumers. As they tend to lend to large corporations, which have stable cash flows, offer collateral and are way more reliable borrowers than average consumers, banks are able to keep their loan default rates at 2%. Good for the banks!

Alternative finance lending companies face the same challenge as commercial banks, they have to be picky in choosing who they lend to, as a lot of borrowers (both consumers and businesses) are not able to repay their loans. As seen from the recent UK based marketplace (real estate) lender “Lendy”, alternative finance companies are not immune from going bankrupt and irresponsible lending may eventually cause the platform distributing loans to declare bankruptcy. “Lendy” currently has £160 million ($203 million) in outstanding loans, over £90 million ($114 million) of which are in default. It means that a lot of investors can lose most of their money invested in the real estate loans on Lendy platform. And Lendy will join the list of its’ predecessors who failed: GraduRates, Fruitful, Encash, First Great National, Quackle, Wellesley & Co, TrustBuddy and etc.

Crash of P2P lending platforms in China

Source: bloomberg.com

Yet another example of irresponsible lending. China has seen a lot of similar P2P lending platforms go broke over the years. The chart from Bloomberg tells it all. Lack of regulation and transparency, as well as careless lending done by these platforms cause them to go broke and investors to lose their money with little or no hope to get it back. As a result, regulators in China want to ban such online P2P lending sites. Thus, $192 billion peer-to-peer lending industry may shrink immensely, and only a handful of platforms (strictly regulated by China regulatory watchdog) will survive.

Everybody gets hurt due to lack of responsible lending

Not only lenders go broke as a result of irresponsible lending. Investors lose their money and trust in lending institutions. If companies or individuals who took the loans were not efficiently evaluated in terms of their credit rating, indebtedness, cash flows, collateral and other factors that help to define how solvent they are, the borrowers (both businesses and consumers) will likely go bankrupt in the long run (which will again hurt the lenders and investors who have put funds in these loans).

The hurt may even be more profound if we take into consideration payday loans. Most customers of payday lenders are mainstream workers with the lowest annual income. The vast majority of them do not qualify to get credit cards, have a very poor credit score, lack access to credit, and face regular financial problems. As interest rates with payday lenders are extremely high (in the hundreds % per annum), the borrowers do get hurt when the aggregate amount they owe to the lenders grows at geometrical progression.

What makes Debitum Network a responsible marketplace?

Debitum Network cooperates with their partners loan originators who offer loans as assets to be invested in on the platform. We carefully select which assets to upload and which ones to reject. We have onboarded third-party partners who are professionals in risk scoring and they do thorough scoring of the borrowing companies and provide their unbiased decision to us. After risk scoring is done each borrower gets a risk score, from A to F (Credit scores used on Debitum Network have been assigned based on a standardized probability of default of the business during the next 12 months). We reject anything below C (D-F) as these ratings indicate that the likelihood of a borrower to go broke within the next 12 months if very high. A to C ratings show that the likelihood of bankruptcy is very low. There are a few assets on the platform with a rating of D-E. They are placed on the platform as the borrowers pledged collateral as a guarantee, and the broker offers a buyback guarantee for the asset. Thus the safety of investing in the assets is increased to the maximum.

Buyback guarantees from the brokers (loan originators) is another measure that helps to keep the lending process responsible. It means that if the borrower is late with the repayments by more than 90 days (the term depends on the loan originator), the broker that issued the loan will have to buy it back with all outstanding principal and interest. This is a strong safeguard for investors’ money. There have been a few cases when the loans were bought back and investors got all of their outstanding principal and interest. It proves that the safeguard is working and investors’ funds are protected. Furthermore, a buyback guarantee is a serious obligation on lenders behalf to evaluate each potential borrower and his creditworthiness accordingly. Too many defaulted loans would sink a loan originator and he would not be able to fulfill his obligation to buy back the loans (as we saw in the case of Eurocent loan originator on Mintos platform). In the period of 9 months, there hasn’t been a single default on Debitum Network platform and investors’ got their invested funds plus interest in full!

Thus, careful evaluation of borrower’s credit history and a buyback guarantee significantly reduces the risk of defaults on Debitum Network platform. These measures protect investors’ funds and ensure their returns on investments do not shrink. They also protect loan originators from the risk of going bankrupt in case too many borrowers default and the loan originator has to buy back the defaulted loans. It also helps Debitum Network to offer the safest possible assets and keep on growing.

A sample asset from Debitum Network to invest in

The asset comes from our reliable partner and loan originator Chain Finance. The loan is issued for the company that specializes in the re-sell of authentic branded products for customers in over 100 different countries and has been operating in the market for over 7 years. It has over 50 employees and over 500,000 EUR in revenues. The asset is protected by the buyback guarantee and has the highest credit rating on the platform, which means it is one of the safest assets to invest in. Check it out.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.