Investments in business loans versus consumer loans

Investments in business loans versus consumer loans

High-interest rates remain the key factor which attracts people to invest in assets on alternative finance platforms (P2P or P2B/B2B). Low-interest rates in the banks have driven people to search for alternative ways to put their money to use instead of keeping them in savings accounts for ridiculously low returns. P2P and P2B lending platforms offer way more appealing options to gain returns than most other investment solutions around. However, promised returns may not be the delivered ones. Let us look at what impacts the real returns and why investing in business loans might be a better option than consumer loans.

How are business loans different from personal/consumer loans?

Business loans are issued solely for businesses and for business purposes. They can be secured (company’s assets are pledged as collateral to be used in case of failure to repay the loan) or unsecured (no assets are pledged as collateral and the lender can only make a general claim for the assets of the borrowing company). Secured loans, naturally carry smaller risks and, consequently, have smaller interest rates.

Consumer loans are personal ones and are issued for private individuals, typically for non-business purposes (buying a home, car, covering social security liabilities, paying of bills). If an individual fails to pay off the loan, the lender will come after his/her personal assets to get back the lent money. As lenders usually have collateral from businesses they won’t require personal guarantees from business owners, which they would do from individuals taking out a personal loan.

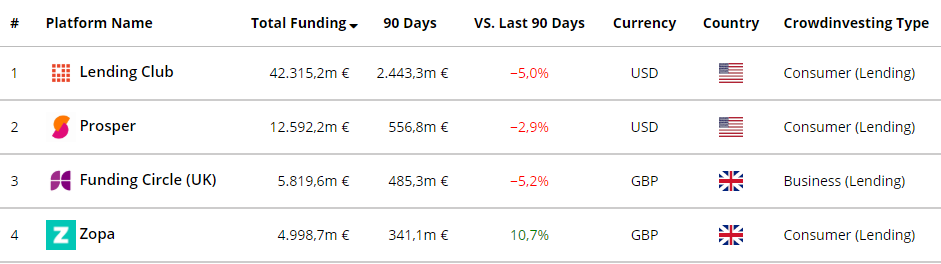

Some facts about the leading P2P/P2B lending platforms

Source: p2pmarketdata.com

According to P2PMarketData.com out of 74 top P2P lending and equity platforms (Debitum Network included) about 20 focus solely on consumer lending. Among them the leaders in volume and total financed loans (Lending Club and Prosper) in the US. 12 of them do both, but with a tendency to offer more consumer loans (leading platforms: Mintos, Twino). 17 belong to Real Estate (Lending) with Sharestates (in the US) and Octopus Choice (in the UK) being the leaders in the sector (we will do comparisons with these platforms and business lending in future posts). 23 platforms focus solely on offering investments in business loans (Funding Circle from the UK being the leader of the group of platforms and our own Debitum Network belongs to the group too).

What are the risks of investing in consumer loans?

Independent reviewers state that investing in consumer loans, even on the most secure P2P lending sites such as Lending Club or Prosper can help you make a 15% return on your investment or cause you to lose money. How is that? The answer is quite simple, different loans perform differently. Some borrowers go bust and they never pay back. Investors typically lose money on these type of loans. Unlike businesses private individuals may not have cash flows to offer, or valuable assets as collateral and the ones that are offered are often not enough to cover the principal of the loan, to say nothing of the outstanding interest. Thus an expected 15% return on investments in consumer loans may be significantly slower and if an investor picks non-performing loans he may not make any money, but lose all of his investments.

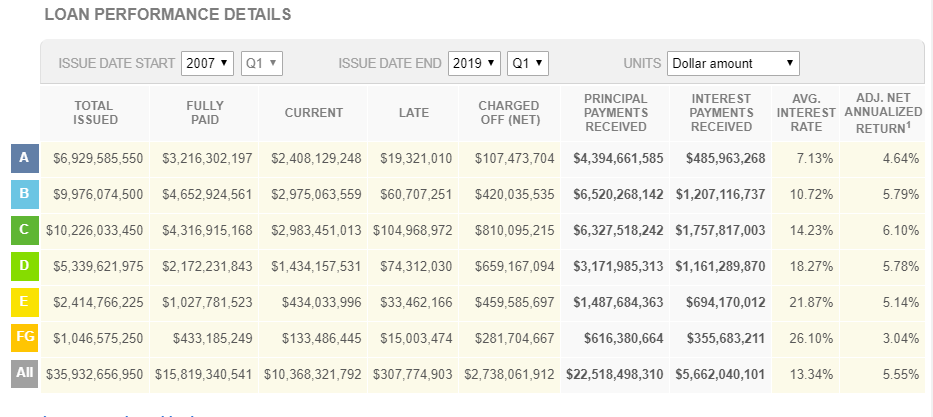

Most of the lending sites rate their loans and the loans with the lowest risk get the lowest interest rates, and the worst risk rate loans get the highest interest rates, some might be as high as 30%. However, even low-risk loans sometimes underperform and default. It takes thorough analysis, wide range classification, and insight to select the most secure loans to get a conservative 5%-7% adjusted annual return on the investments. Lending Club (one of the most trusted P2P lending platforms) gave this table to show how average interest rate may differ from adjusted annualized return for investors.

Data source: https://www.lendingclub.com/info/demand-and-credit-profile.action

Data source: https://www.lendingclub.com/info/demand-and-credit-profile.action

What about the risks of investing in business loans?

The main risk of investing in business loans is the same as that of investing in consumer loans – a loan may default and investor lose all of his invested money. So, why not invest then in consumer loans if they offer higher interest rates? The question is logical and it has the logical answer. Business loans are inherently safer to invest in as they will offer more safety for investors’ funds. A business may pledge collateral (equipment, warehouse, cars, goods), invoices as a guarantee that the loan will be fully repaid. In case of borrower’s failure to pay off the loan, the lender can go after the assets of the borrower and get back the principal and interest due on the loan (in the best case scenario).

On some platforms (Debitum Network included) loan originators that upload their assets on the platforms also offer a buyback guarantee for the loans they have issued. This means that if the borrower is late with the repayment of the loan by a specific number of days (typically 30-90 days), the broker who issued the loan will have to buy back the outstanding principal and the outstanding interest. This reduces the risk of investing in business loans on the platforms to the minimum.

Under these conditions, the real possible risk from the possibility (a rare one) that the loan originator will go broke and fail to buy back the principal and outstanding interest. It happens from time to time as in the example of the loan originator Eurocent (on Mintos platform), when investors lost their money invested in the loans issued by the mentioned broker. Despite the efforts of the platform to get back investors’ funds, the hope of positive outcome seems to be dim. Thus, the buyback guarantee is as good as the loan originator that provides it.

How safe is investing in business loans on Debitum Network platform?

However, these events are rare and lending to businesses with the protection under a buyback guarantee provides investors with maximum safety. In the period of 8 months since the launch of Debitum Network platform we have uploaded hundreds of loans to choose from, and there hasn’t been a single default. Thus, investors have got back all of their invested principal and earned interest. Plus, late loans give investors an opportunity to earn extra profits from existing penalty rates (those differ among loan originators and specific loans), thus increasing his/her profits along the run. At the time of writing, the average interest rate paid to investors on Debitum Network platform is 9.72%.

Want to earn attractive interest on Debitum Network assets?

We regard the safety of investors’ funds seriously and take only the best assets that our partners loan originators offer. Most assets are short term and this is another safety guard for investors’ capital because borrowers have to prove that they are able to pay off the principal and interest for a considerable term after taking a loan before we accept it on our platform. Short term, also means that your capital is never frozen for a long period of time. Fast turnover and compounding interest is what makes our platform attractive! Want to start investing?

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.