What do investors want?

What do investors want?

Management team of a successful company should treat available capital (the one that can’t be deployed right away) similarly as any investor would do – diversify it among assets, look for solutions over various periods of time, ensure durability of their business. Investment in alternative financing via various platforms like Debitum Network is a great tool for short and medium run money management.

It is one thing to state the fact, that profit-seeking companies aim to earn profit from their activities and generate returns on their assets. It is significantly more complicated to answer how to do it. In this article, I will provide some ideas on the topic of employing the funds we have.

We strive to maximize return within acceptable risk boundaries with minimal effort in the medium – to – long run.

First of all, it is important to point out that the approach presented here is not necessarily suitable for everyone, and is presented for information purposes only. It is not intended to be investment advice. You should seek a duly licensed professional for investment advice matching your specific situation.

And now let’s unpack it, starting from the end of that sentence.

INVESTMENT THEORY

We talk about the long run investment, and many things fit within this term. There is no specific number of years that would represent the long term, but I propose to think about it as a period of time that is difficult for you to imagine clearly. None of us knows for sure what companies will be attractive in 20 years. Moreover, even if those companies will exist at all by that time. By contrast, medium term is much more certain to happen. We all have specific ideas for significant events a year or two down the road, like forming a new team of developers or moving to a larger office.

“We are hard-wired to want immediate payoffs, even if it is unwise.”

Shahram Heshmat Ph.D. Link

One common feature about the distant future is the difficulty for people to judge probabilities correctly. As a rule, people prefer things they can get “here and now” to something they would be getting later.

Finding the right level of predictability and mitigating risks are essential considerations for any investor who aims to accumulate wealth gradually and long term. In situations where supply is not limited, increase in predictability comes together with a decrease in return, since investors would be willing to commit their money for a smaller rate of return. In other words, if the level of return remains unchanged, more and more investors would be willing to invest in any specific asset as the uncertainty of their investments goes down.

Another issue that has to be taken into account when investing for the long term is a systematic risk (also called market risk) related to the particular investment. Systematic risk incorporates factors that are common for the whole country or industry (e.g., cryptocurrencies): interest rates, regulation changes, recessions, and wars, among others. They can be mitigated only by incorporating assets from multiple markets into the portfolio.

Mutual funds and other “packaged” investment solutions sold by financial institutions is one way to mitigate political, macroeconomic and currency risks. The rising wave of web-based peer-to-peer financing platforms and other distributed solutions provide even more affordable and transparent alternative.

Many investors will tell you that it is not enough to have the right portfolio, it is also very important not to fiddle with it. The minimal effort part is included specifically for this purpose: it is all too easy to get excited about one piece of news or another, yet it is not a good idea to routinely spend time and effort revisiting choices that have already been made.

You need to have enough situational awareness to make well-informed decisions. At the same time remain distanced from the swinging moods of the market. Transaction costs required to make the adjustments in your portfolio (both fees and time needed to make the decisions) would likely eat away a significant portion of your returns.

Unless you are planning to use returns from your investments as your primary source of revenue, you would be better off minimizing portfolio management and concentrating on your primary goals instead.

To be clear, minimal management is quite different from no management, and you should have a grasp how well your investment portfolio matches your personal/company situation and whether the level of risk that you are exposed to is adequate for you. Too much risk can obviously expose you to unacceptable losses that might harm the future for you and even jeopardize the daily operations, but risk can be too low as well: if you enjoy operational income that exceeds your day-to-day costs, don’t have significant expenses in the foreseeable future and keep all the savings as cash or bank deposits you can be quite sure that inflation will start “eating” your savings away and your ability to purchase goods or services with that money will go down with time.

When balancing between safety and returns for your investment you have to take liquidity of your investment into account. A Picasso painting might be worth a lot of money and can be reasonably expected to be worth even more in the future, yet you might find it difficult to sell one or even use it as collateral in case of unexpected and significant expenses.

Eventually, we come to the most important part: having all the above-mentioned considerations in mind, we seek to maximize our returns. It might be tempting to find one single asset (let’s say a promising token in a new ICO) or class of assets (be it cryptocurrencies, or your local real estate) and invest all your spare cash there. Yet the risk is great to lose it all if the value trend of a volatile asset takes the wrong turn. Diversification is, therefore, your first layer of defense: if a single asset fails to provide expected returns or even loses value, you are not risking to lose all your investment funds.

Word of caution – you should not be misguided by the power of diversification or other ways to reduce the risk for you. As a general rule, if something looks too good to be true, it probably is. Here I would like to point out one critical consideration – use of leverage to boost the returns on your investment. It might be tempting on the first glance to borrow from someone at a smaller interest rate and invest into other assets promising higher return thus effectively multiplying returns of your own. While doing this, you must not forget that the ease with which leverage can multiply your returns and ensure great profitability can turn against you and quickly eat up your initial investment. In this case, your investment will serve as a pillow safeguarding the lender that provided you with funds for leverage, but not yourself.

USE CASE – SUCCESSFUL ICO

After reading all of this you might ask – so how do we solve an equation with so many variables, and as I said in the beginning, there is no single one-fits-all answer. However, here is my approach to investing funds for Debitum Network:

I know that the cash we enjoy having today must ensure unrestrained operations for the team developing the Debitum Network platform.

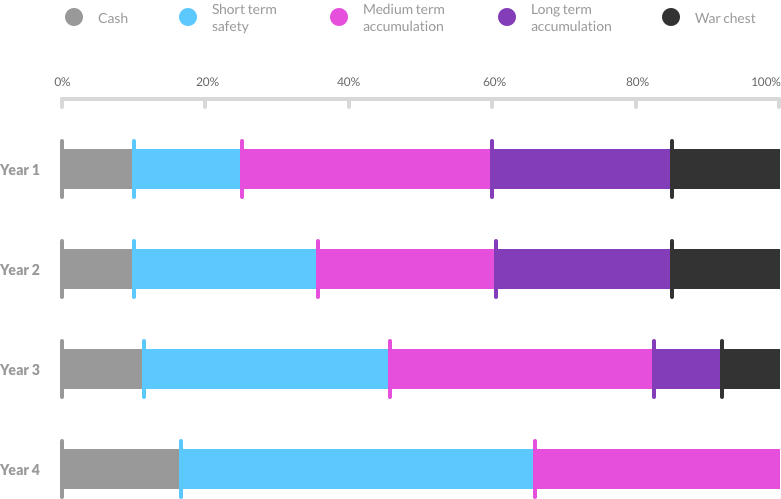

I know that if we do not do anything with the funds and keep it as cash, it will be enough to ensure three years of operations, and I know with near certainty that we need ¼ of the funds for the first year.

Cash

Very high liquidity, of negative return due to exchange rate fluctuation and inflation

- Fiat currencies: your local / USD / EUR / GBP / CNY / JPY

Short run

Clear maturity, modest return (3-6% would be good)

- Interest-bearing bank deposits

- Loans with maturity between 1 and 12 months, Quick loans for leveraged trading

Medium run

Longer maturity, possibility to sell on the secondary market, better return (~10%)

- Loans with maturity longer than 12 months

- Publicly traded bonds

Long run

Assets “frozen” for extended periods of time (5 years or more, with limited possibility of early exit), significant but not certain return (15% and up)

- Investments in equity/real estate funds

Warchest

High liquidity, separated from cash for safety reasons. Possibility to multiply the value of investment: return 2X and up.

- Funds dedicated to the acquisition of significant assets/ entire companies/ spin-off ideas

Part of assets has to stay cash, but money that will be spent half a year from now can still be employed quite safely in the short term. The goal of such investment would be to beat inflation (e.g., in USA 2.5% per year at the time of writing) while maintaining sufficient liquidity that we can use the funds when they become necessary. Which means we can convert any asset in this group into cash within one month from the decision to do so.

Next comes medium term accumulation: the bulk of funds would be allocated here to earn what I would consider medium returns (~10%) while at the same time ensuring continuity of operations as Debitum Network moves towards profitability. When investing for the medium term, I consider assets like bonds with a maturity date within an acceptable time window or assets that I could sell within three months from a decision of doing so.

On top of that, we have long-term accumulation – funds that can be invested into assets with lower liquidity (e.g., real estate fund) knowing that it can take a few years to get the money back but promises us higher returns (15% or more).

And finally, we have our war chest portfolio, funds that can be used to fund new features or additional business ideas to improve Debitum Network platform and to bring more value to the ecosystem. We would keep funds in fiat with high volumes of trading to ensure liquidity, yet returns on these funds would be highly uncertain, having the potential for 2X or even higher returns.

The graph below represents the allocation of funds among these classes in the extreme scenario where we do not consider any income from Debitum Network operations. Not the absolute amounts, but portfolio composition is important for this analysis. Due to the gains on our investments, we have availability to finance operations for Year 4.

OPPORTUNITY WITH DEBITUM NETWORK

There are multiple options available from classical assets offered by Banking institutions to B2B and P2P financing solutions (Debitum Network, Mintos, Twino, Funding Circle or Lending Club) that are spearheading the area of new investment assets. As these assets get closer to meeting the needs of current day businesses they attract more investors which brings the overall level of uncertainty down.

There are several business-to-business financing platforms available that offer these new types of assets. Businesses are liberated to offer financing contracts and set them to meet market needs. Change of the rate of return, duration, underlying collateral – everything can be updated as needed and almost instantly. For investors like me, this means higher diversity of assets, the ability to investigate all the details of those contracts, and choice to select the ones that fit our needs.

Once operational (planned release in September 2018) , Debitum Network platform will be a great solution for the short and medium term fund allocation: known duration of loans, third-party risk assessment, the possibility to invest into loans originating from multiple countries and industries, as well as attractive interest rates will make Debitum Network platform a welcomed addition to any portfolio.

If there is one thing certain when thinking about the future, it is that things rarely remain constant. And just like the supply of funds from investors is rising, demand for financing from SMEs is growing too. This growing economy provides ample opportunities to invest.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.