Why borrowing money could be a good thing for business?

Why borrowing money could be a good thing for business?

Getting into debt is a situation that most businesses would rather avoid. However, there are some instances when getting into debt is unavoidable – and actually good for your business. It is obvious that there are not only bad debts but also good ones. Some companies borrow and fail, others get into debt and succeed. Growing your business might be one of the reasons when getting into debt is not only advisable but probably a must.

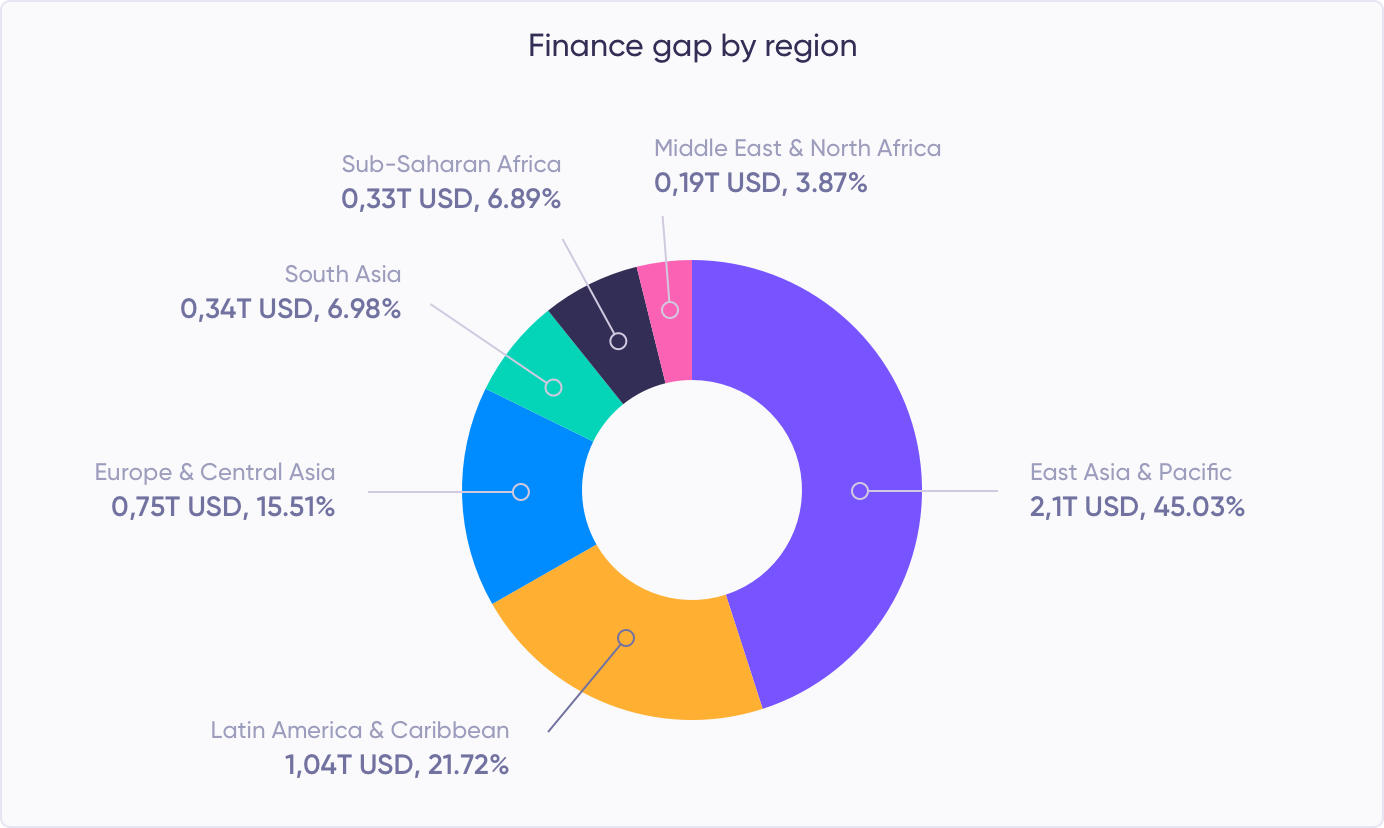

The fact is that most businesses go bankrupt due to lack of access to credit more than for any other reason. This proves the necessity of responsible borrowing and lending. The chart from the SME finance forum indicates that small businesses around the world badly need access to credit. The current credit gap for SMEs globally is 5.2 trillion US dollars (from 2.2 trillion US dollars 2 years ago). Thus, businesses need to borrow now more than ever.

Source: smefinanceforum.org

The difference between good and bad debt

Debt in itself is neither good or bad. It may become one or the other depending on how the borrowed money is used. Bad debt is usually the one when the borrowed funds are used to purchase depreciating assets, or the usage of the borrowed money does not contribute to business growth. If it does not serve the purpose of generating income in the long run, it would fall into a bad debt category too. If borrowed money generates more money, helps to increase income, net worth, expand and growth business, this type of debt is considered good. So, if your business borrows money to make more money it might be considered good debt.

When should businesses take a loan?

To cover start-up costs

Before a business can sell something, it needs to have what to sell. It also needs some items before it can start operating (cell phone, computer, some stationary goods or a car). In most cases, it would need way more: stock, office to work from, resources for a marketing campaign, and money to pay the staff, even if it is a company consisting of a few people.

The money to buy that (or pay for that) should come from somewhere. It may be personal resources, a loan from a family or from a lending institution. It does not matter where it comes from, the fact is: it has to come from somewhere and a start-up company should consider getting a line of credit one way or another.

Generate more profits to cover the cost of borrowing

A lot of companies, even very profitable ones continue borrowing with the intention of increasing sales and growing their businesses in order to generate enough profits to cover the costs of borrowing. If more money is generated with the borrowed funds than it costs to borrow, it is worthwhile for businesses to borrow.

Let’s say the purchase of inventory cost you 10,000 Euros and the extra interest on the loan is 2,000 Euros. Is it worth it? It depends on the return. If it is 50,000 euros, it means you have to pay 2,000 euros to get 38,000 euros. That’s is an excellent deal and paying 20% annual interest is not an issue at all (due to such high returns). This is how businesses make the best of debt and use it to make profits.

The table below helps you to decide whether it is worthwhile to borrow or not. Apparently, 3 situations are good for borrowing and one could be categorized as a bad debt. A rule of thumb remains the same: if the potential investment on the return outweighs the debt, go for it.

Get working capital to increase cash flows

Working capital is very important as it enables the company to pay short-term expenses or debts. Suppliers and employees have to be paid. Lack of working capital puts pressure on the cash flows of the company. If the company is really profitable, it can finance its’ working capital out of its’ profits. However, not every company is, and most companies willing to function unobtrusively have to get working capital. A short-term loan is one of the best options to get it.

Keep operating during the slow season

A lot of businesses, particularly those in retail are seasonal in nature. If they make most of their income during a particular season and their business stalls in other seasons, they want to purchase inventory prior to the active season begins. Thus, they will need funds to continue their operations during the months of low business activity and purchase inventory for the upcoming active season. These loans will be short term and will typically be paid off after the active season is over.

A few considerations before taking a loan for your business

Before you take a loan you should ask yourself a few questions. First and foremost, can you service the debt? You need to have a plan on how you are going to pay off the loan and the interest. If your calculations show that the debt might sink your business, the best path to follow is not to take it. The second one is: can you make a profit as a result of borrowing? We’ve already discussed that the positive answer to the question means you should definitely borrow.

Investors on Debitum Network can participate in financing short term loans for SMEs

Private and institutional investors can register on Debitum Network platform and contribute to the global growth of small businesses by investing in short term loans for SMEs while earning attractive interest at the same time. Minimum deposit amount is 50 euros, the minimum investment amount is just 10 euros. The platform has been recently redesigned from square one and you can try investing on the BETA version of Debitum Network 2.0 now.

The top asset of the week selected for you

The top asset this week comes from our reliable partner and loan originator Factris Lithuania. The borrowing company hires, trains and equips workers for scaffolding activities in foreign markets, it has revenues of more than 4.4 million EUR and employs more than 30 people. The management of the Company has a cumulative experience of more than 15 years. The Purchaser of invoices is a large and profitable European company which is controlled by a holding company, which has assets over EUR 1.1 billion. Check out the asset.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.